Should you trust your hard-earned retirement portfolio to a robot?

The math doesn’t lie. The answer is a resounding NO.

All automated investment services, or ‘robo-advisors’, have the same value proposition. They are easy, low-maintenance, automated investment advisors. They use algorithms to set a predetermined proportion of your portfolio in basic index exchange-traded funds after a series of questions to determine customers’ risk tolerance. The algorithm then recommends a diversified portfolio and does this automatically. If you contribute $10,000, it will allocate X% to US stocks, Y% in foreign stocks, and Z% into emerging markets, and so on.

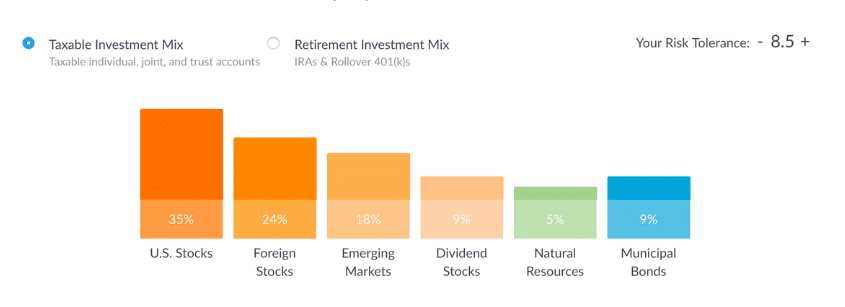

To give an example based on my own risk tolerance, this is what my portfolio would look like on Wealthfront.

These services have quickly amassed billions of dollars in assets under management (AUM) from young professionals. Wealthfront reached $20 billion AUM as of September 2009, Betterment had $16.4 million as of April 2019. They market their platforms on Nobel Prize winning research to build their models. In reality, they just tell investors to buy simple index funds.

Before diving into some research, I actually think the idea is brilliant. Investors contribute, the platform takes care of the rest for a small annual advisory fee of 0.25%. For this fee, the platform promises to lower your taxes, using strategies like “tax-loss harvesting”, and to manage your risk. On top of these annual fees, investors need to pay the individual index fund expense ratios that invest into their portfolio. This model is a great deal for companies like Wealthfront. They attract young, ignorant professionals early and invest their money for the rest of their lives, skimming larger and larger fees from their accounts as their wealth grows.

The dirty little secret is most investors do not have a grasp of compound interest. They certainly do not understand how compound fees work.

If a 25-year old invests $100,000 of retirement funds with Wealthfront, they will likely pay the company over $100,000 in fees by their 66th birthday.

If they invest additional money from their salary over that time, the fees will grow even higher.

You might say, “I don’t want to invest myself. I would rather have someone do it for me.” I can’t fault you for wanting to pay for convenience. I have good news for you. Vanguard has what’s known as Target Retirement Funds. These are automated investment vehicles that rebalance overtime, adjusting for risk as you grow older based on your intended retirement date. In my case, the Vanguard Target Retirement 2055 Fund is what I would choose.

This is basically Wealthfront without a 0.25% fee charged on top of your account. You will not be able to avoid fees entirely, but in Vanguard’s case – they are quite small.

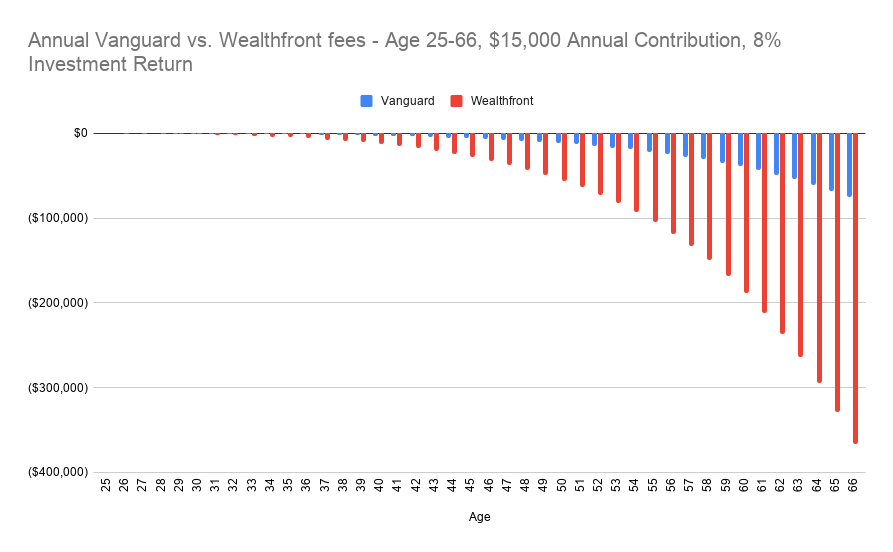

I’ve built a simple model to show the differences in portfolio values and costs if you invest without fees, if you invest in a simple low-cost option with Vanguard, or with a robo-advisor service. As you will see, the cost of using a robo-advising service like Wealthfront and paying 0.25% over time adds up significantly. How significantly? Spoiler alert: it’s a lot.

Let’s take a look at some examples.

In the first scenario, let’s assume a $10,000 initial investment, a $5,000 annual contribution, and a 7% investment return. 10 years after starting the investment, the fees are not that large. These fees start to compound and get much larger later down the road. By the time you reach retirement age and are ready to use these funds, you will find out that the robo-advisors have taken over $100,000 of your investments over the years through the 0.25% they charge.

How is that possible? Every time you pay the 0.25% fee to the robo-advisor, that money is no longer yours to invest and grow at a compounded rate. It might not seem like a lot at first, but it’s significant over a 40 year investment career.

If you’re an aggressive saver and a successful investor, the magnitude of these fees will be even worse. Our second example will assume the same $10,000 initial investment, but this time the annual contribution will increase to $15,000 and the investment return will be 8%. By the time you reach retirement age, the robo-advisor will take over $350,000 from your account.

Are robo-advisors a scam? Well, not in the Bernie Madoff sense. But I don’t see how investors do themselves any favors by investing this way. These robo-advisors do not promise to outperform the markets any more than a regular index fund. Personally, I would not invest in something knowing the long-term impact the fees will have on my wealth. As Ramit Sethi wrote in the terrific personal finance book, I Will Teach You To Be Rich:

“Most of us have been taught to ask $3 questions. We should really be asking $30,000 questions.”

Or in this case, $300,000 questions.

Note: If you’d like to receive future articles by email, subscribe to my Wednesday Wisdom newsletter.

Acknowledgements: Thanks to Adam, Ben, John, and Blair for their feedback on this post.

The trouble with your analysis is that it does not take into account tax loss harvesting. I have $75,000 in Wealthfront now, I have paid $58 in fees, it claims it has saved me $352 in taxes through tax loss harvesting. Does considering this alter the math at all?

LikeLike